[email protected]

English

Home

About KPRA

Performance

Performance Overview

KPRA vis-a-vis FBR

Major Sectors

About

About KPRA

Governance Structure

Organizational Structure

Strengthening Legal Framework

Strategy Formulation

Mandate of KPRA

Human Resource

Collectorate of Appeals

Introduction

Function and Power

Officers and staff

Pendency and disposal statement

Library

Appeal Before Collector (Appeals), KPRA

Key Initiatives

Broadening of tax base

IT Enabled Taxpayer Support Services

Awareness Campaigns

Training of withholding Agents

Messages

Message from Chief Minister

Message from Advisor on Finance

Message from Director General

Taxpayer Guide

How to Register

Documents Required for Registration

Change in Particulars Request

Affidavit for Registration with KPRA

E-Registration

How to E-Register

How To E-Enroll

E-Registration Video Guide

Relevant Tax Rates

Rates applicable on each service

Rates of Sales Tax in KP

Tax Returns Filing

E Filing Annexure Submission

How to E-file STS Return (English)

How to E-file STS Return (Urdu)

How to File Null Return (Video)

Tax Payment

How to Pay STS Online

Media

Gallery

News & Updates

KPRA TV

Jobs & Career

Tenders

Downloads

Legislation

Acts

Notifications

Rules and Regulations

KPRA Annual Reports

KPRA Annual Report 2022-23

KPRA Annual Report 2021-22

KPRA Annual Report 2020-21

KPRA Annual Report 2019-20

KPRA Annual Report 2018-19

KPRA Annual Report 2016-17

Other Links

KPRA RIMS

Application Forms

User Guide

Required Documents for KPRA Registration / SOP

Appeals and Orders

Appellate Tribunal

Collector Appeals

Compulsory Registered Taxpayers

FAQs

Contact Us

Reward Scheme

Consumer Reward Scheme

Verify Invoice

KPRA RIMS

E-SERVICES

E-Services

English

✕

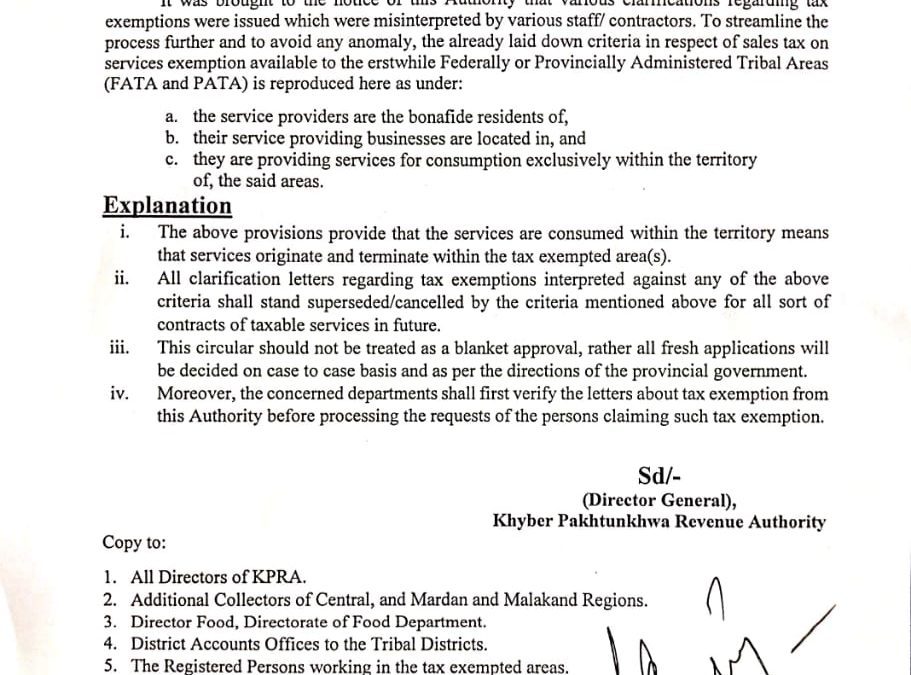

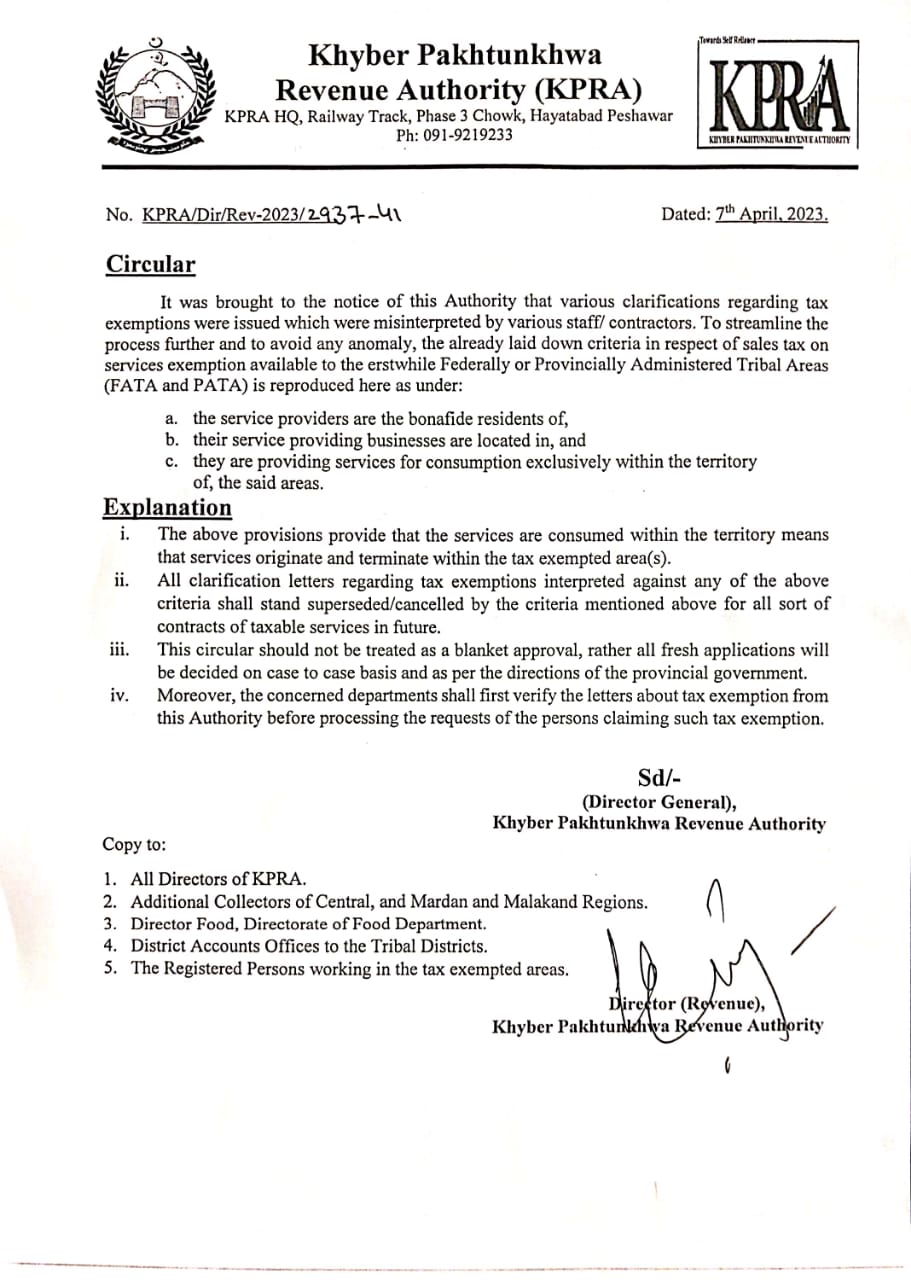

Circular: Clarifications Regarding Tax Exemptions of FATA/PATA

Circular: Clarifications Regarding Tax Exemptions of FATA/PATA

Published by

Mr. Gohar

on

April 10, 2023

Categories

News

Tags

English

No translations available for this page

0

0